Gold is, in fact, a poor hedge against inflation. Accounting for changes in the cost of living, gold has returned an average of minus 0.4% annually since 1980, versus positive annualized returns of 7.9% for U.S. stocks, 6.2% for U.S. bonds and 1.2% for cash, according to Prof. Spaenjers.

1980, you say? I wonder how Prof. Spaenjers chose that starting point.

Oh, this.

Of course you can make returns look bad if you cherry-pick the absolute worst starting point!

There is absolutely no exception for going for a walk or run or bike ride to get exercise and fresh air. But trips to the drug store, food store, and even to get restaurant take-out are allowed because food supply and other necessities fall under the critical infrastructure exception.

That's crazy. If you want to go out for a walk alone for exercise, you have to crowd into a store as a pretense! This idiot is going to cause people to spread Coronavirus more!

Fortunately, Newsom's public statements indicate that he didn't read or understand what he signed. Union-Tribune:

Newsom asked Californians to practice social distancing when performing such “necessary activities.”

“We’re going to keep the grocery stores open,” he said. “We’re going to make sure that you’re getting critical medical supplies. You can still take your kids outside, practicing common sense and social distancing. You can still walk your dog.”

In this age of government by morons, I'm going to assume the more lenient of the conflicting statements wins.

As part of a forthcoming package of proposed tax cuts, the White House is considering ways to incentivize U.S. households to invest in the stock market, according to four senior administration officials familiar with the discussions.

The proposal, one of many new tax cuts under consideration, would see a portion of household income treated as tax-free for the purposes of investing outside a traditional 401(k). Under one hypothetical scenario described by multiple officials, a household earning up to $200,000 could invest $10,000 of that income on a tax-free basis, although officials noted these numbers are fluid.

CNBC's Kayla Tausche, like her colleague Brian Sullivan, is a blithering idiot:

Money put into the account would be done so on an after-tax basis, and taxed when withdrawn as well; but any accumulation of profits during the investment timeframe, known as capital gains, would not be taxed.

No, an accumulation of profits is not "known as capital gains." The accumulation of profits comes from both dividends and capital appreciation. Capital gains are taxed only when a position is sold. Tausche doesn't mention how dividends are treated, though they make up the vast majority of the "accumulation of profits" for low-turnover investors.

The proposed accounts arguably aren't of much value. Capital gains are already deferred for buy-and-hold investors. And even realized capital gains and dividends are taxed at low rates. Being taxed at ordinary income rates upon withdrawal will likely make these accounts a worse deal than just buying index funds or ETFs in a taxable account. Which, by the way, you should already be doing.

On today's radio program, a caller asked about children needing earned income to contribute to IRAs. He wanted to be able to start his kids investing early to take advantage of many more years of compound growth. Edelman suggested that the caller pay his kids as employees for chores, issuing them an IRS 1099 form and creating earned income eligible for IRA contributions.

That's one option, but there's another that's almost as tax-advantaged for kids and less restrictive. You can open a taxable custodial account for kids (called UGMA or UTMA) at any brokerage like Charles Schwab or Fidelity. You can give the kids as much as you want up to the gift tax limit (currently $15,000 per parent or other giver per year). You can then invest in whatever stocks, ETFs, or funds you want.

For kids, a taxable account is essentially as tax-advantaged as an IRA. Kids get the minor unearned income exemption, currently $2,200 per year. With dividend yields below 2% and little capital gains from index funds, that makes the account essentially tax-free until it gets really big. And you can even realize gains tax-free in order to step-up the cost basis.

Assuming we're talking about a Roth IRA (there's little point in using a traditional IRA for a child in a zero or very low tax bracket), here's how a taxable account compares to a Roth. You get much bigger contribution limits and more flexibility for withdrawals. And the tax treatment is quite similar until the account grows large or the child grows up and is in higher tax brackets as an adult.

Roth accounts' permanent tax-free treatment (at least unless Congress changes the law) still has the edge over taxable accounts if the money is meant for retirement. But why not do both? Open a Roth, but also put some money in a taxable account that is essentially tax-free in the early years and can be used for college or a first home purchase or anything else in the early adult years.

Disclaimer: The W.C. Varones Blog is not a CPA or a tax adviser. Always consult your own tax professional.

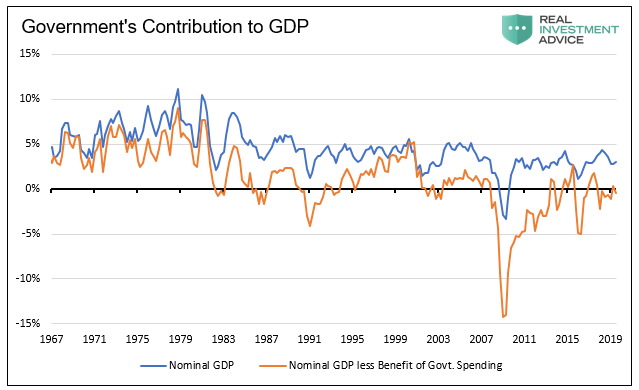

As shown below, when one strips out the change in government debt (the actual increase in U.S. Treasury debt outstanding) from the change in GDP growth, the organic economy has shrunk for the better part of the last 20 years.

Data St. Louis Federal Reserve

The argument is that since deficits flow directly into GDP via

GDP = C + I + G + X

(an increase in Government spending mathematically creates an equal increase in GDP), and deficits (~5% of GDP) are greater than GDP growth (~2% real growth), then GDP (i.e. the economy) is actually shrinking if you back out the contribution from deficit spending.

The argument has been made by others, including Karl Denninger, and forwarded approvingly by John Mauldin. I've even made the claim myself on Twitter.

Seems legit, right?

The problem with the argument is that it confuses the level of the deficit with the change in the deficit.

The deficit affects the level of GDP. The change in the deficit affects the change in GDP (that is, GDP growth).

To illustrate, assume we have been running somewhat constant 5% GDP deficits, similar to the current situation. Now assume we immediately stopped deficit spending and ran a balanced budget. GDP would immediately decline by 5% for that year. But what would happen next year with another balanced budget? The GDP would not experience another 5% contraction from austerity. It's the change in deficit, not the level that moves GDP growth. The chart above gets this exactly wrong, showing that somewhat steady 4-5% deficits create continuing declines in the "ex-deficit" economy.

None of this, of course, is to say that our current path of perpetual deficits greater than GDP growth is in any way sustainable or a good idea. It's not! But we're not shrinking, and we wouldn't perpetually shrink in the absence of deficits.

So we're going to get essentially another Clinton impeachment acquittal: he did it, but we're not going to remove him because it's not that serious and he's kinda popular.

However, if you look at the distribution of ownership of stocks/401ks/IRAs, I think you'll find that a few rich hold a LOT of stocks, enough to live off dividends without liquidating.

The broad masses have little or no stocks and will work longer and/or live off Social Security and home equity.

It's only those in between we need to worry about liquidating, those with a few hundred thousand dollars in 401(k)s. Are there that many non-rich that hold enough stocks to impact the market when they sell? Sure doesn't look like it.

Now sure there are traditional defined-benefit pensions too, but public pensions are still growing and underfunded, and need to keep accumulating. Private pensions are relatively small and hold low stock allocations. So where is this generational liquidation going to come from? I just don't see it.

One of the respondents offered the following story:“It has been a difficult time for our family, my wife is now on medication for depression. The stress of being trapped in a mortgage and struggle to manage monthly has had a devastating impact.

“My sister, who was in a similar position, [had a] marriage end as her husband could not manage financially. She sadly committed suicide in June. We have no doubt the mortgage mess they were in played a huge role in her mental health deterioration.”

Everyone who does retirement planning thinks about about asset allocation. But often overlooked is the importance of tax diversification. It's a good idea to have all three categories of account (taxable, tax-deferred, and tax-free Roth) so that when you retire you'll be able to draw from whatever accounts make the most sense based on (currently unknowable) future tax law and your future tax bracket.

But efficient planning goes beyond just having some money in all three account types. It also matters where you put different types of investments. Charles Schwab has a good article on tax-efficient investment placement here:

As a general rule, investments that tend to lose less of their return to taxes are good candidates for taxable accounts. Likewise, investments that lose more of their return to taxes may be better suited for tax-advantaged accounts. Here’s where you might consider placing your investments:

Everyone knows not to put munis or annuities in a tax-deferred account, but not everyone thinks of putting REITs in a Roth. REITs aren't taxed at the corporate level, because they pay out a required portion of their earnings as taxable (ordinary income) dividends. But if you get those dividends in a Roth, they're never taxed. The higher ordinary income tax rate on REITs makes a Roth (and, to a lesser extent, a traditional tax-deferred account) even more advantageous for REITs than it is for stocks.

There is one area that Schwab's article misses: foreign stocks (and funds and ETFs of foreign stocks). They should be in your taxable accounts, because you get part of your dividends withheld as tax by the companies' home countries. In a taxable account, you get a credit against your US taxes for the amount withheld. In a Roth, those withheld dividends are lost forever. And even in a traditional tax-deferred account, reclaiming withholdings can't be done until you take distributions and requires decades of record-keeping. It's so cumbersome I suspect few retirees bother.

When choosing your asset allocation, also remember to choose the right accounts!